Secure Payment Process for Contractors: A Homeowner's Guide

TL;DR:

- A secure payment process for contractors involves verified onboarding, milestone-based fund releases, and fraud prevention protocols to protect homeowners and contractors. Escrow accounts and lien waivers ensure funds are safe and properly verified before payments, reducing disputes and fraud risk. Proper documentation, phone verification of banking changes, and automation are essential for successful, trustworthy project payments.

A secure payment process for contractors is defined as a structured system of verified transactions, milestone-based releases, and fraud prevention protocols that protect both homeowners and contractors throughout a renovation or maintenance project. Poor payment practices cost homeowners far more than convenience. 88% of businesses report that secure, faster payments directly enable growth by building trust and reducing fraud risk. For homeowners managing a bathroom remodel, roofing replacement, or electrical upgrade, contractor payment security is not optional. It is the foundation of a project that finishes on time, within budget, and without legal disputes.

The core tools in any reliable payment process include escrow accounts, milestone payment structures, vendor onboarding documentation, and multi-channel payment verification. Each one addresses a specific failure point. Escrow prevents fund misuse. Milestones tie money to verified work. Onboarding catches fraud before it starts. Verification stops ACH redirection scams before a single dollar moves. This guide walks you through each layer, step by step.

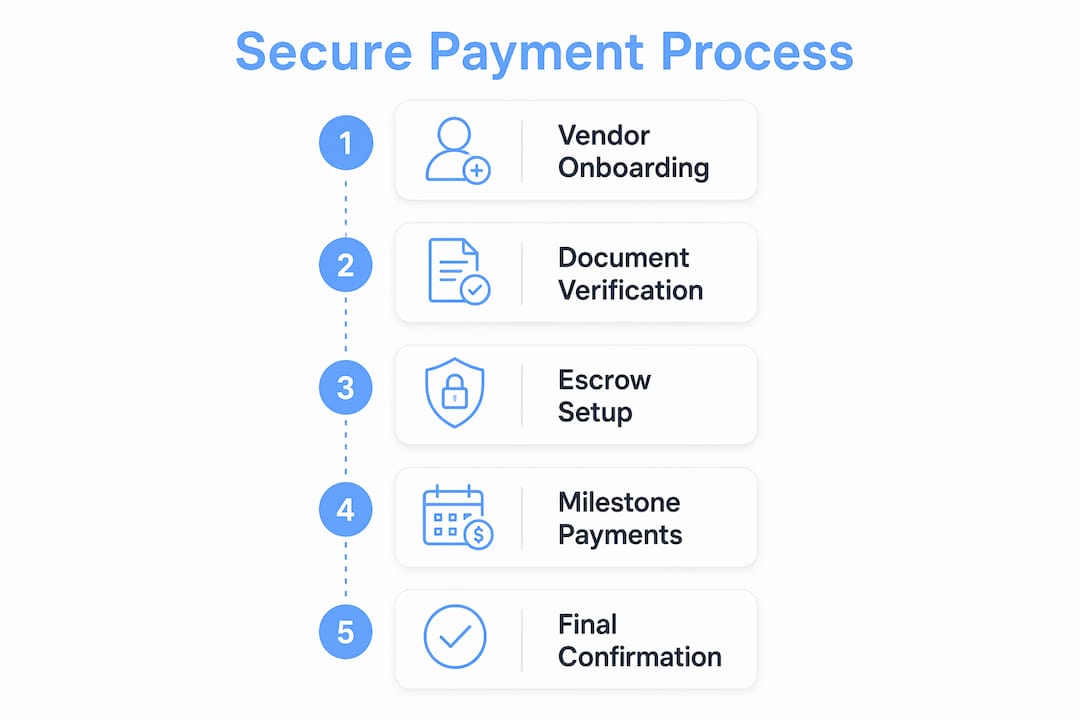

What does a secure payment process for contractors actually require?

Setting up a secure payment process starts before the first check is written. Vendor onboarding is the formal process of collecting, verifying, and recording all contractor information before any payment is authorized. Skipping or rushing this step is the single most common mistake homeowners and project managers make.

Collecting the right documents from day one

Every contractor you hire should provide a completed W-9 form, a signed ACH authorization form, proof of a valid contractor’s license, and a current certificate of insurance with your name listed as an additional insured. These are not bureaucratic formalities. They are your legal protection if a project goes wrong, a subcontractor files a lien, or the IRS sends a penalty notice.

Incorrect 1099 setup can trigger $280 per form in IRS penalties if not corrected within 30 days. That is a direct financial consequence of skipping proper W-9 collection. Use IRS TIN Matching to verify every W-9 before you process a payment. This free IRS tool confirms the contractor’s name and tax ID number match federal records, which protects you from penalties and confirms you are paying a legitimate business.

Verifying licenses and insurance before work begins

A contractor’s license number should be verified through your state’s licensing board website. In Texas, the Texas Department of Licensing and Regulation maintains a public database for most trades. Insurance verification goes one step further. Request a certificate of insurance that names you as an additional insured, not just a certificate holder. This distinction matters because additional insured status gives you direct coverage under the contractor’s policy if a claim arises.

Lien waiver collection must start with the first payment. Exchange unconditional lien waivers only after payments have fully cleared. This preserves your leverage throughout the project and prevents subcontractors from placing liens on your property for work the general contractor was already paid to cover.

Setting up your accounts payable system correctly

Errors in AP system configuration cause payment delays and reporting problems that compound over time. Before you process your first contractor payment, confirm that vendor master records, tax setup, and payment terms are correctly entered. Test your payment workflow with a small transaction before releasing large milestone payments. This one step prevents the kind of configuration errors that delay payments by 7 to 14 days and generate late payment interest on large contracts.

Pro Tip: Never accept banking information changes from a contractor via email alone. Always confirm any change to routing or account numbers with a direct phone call to a number you already have on file, not one provided in the email.

How do escrow and milestone payments protect your project funds?

Escrow accounts and milestone payment structures are the two most effective tools for contractor payment protection in renovation projects. They work together to guarantee funds are available, released only for verified work, and managed by a neutral party.

How escrow accounts work in construction projects

Escrow accounts separate project funds from a contractor’s general operating account, preventing fund misuse and protecting your capital if the contractor faces financial trouble. A neutral third-party escrow agent holds the funds and releases them only when agreed conditions are met. This structure gives homeowners legal separation between their money and the contractor’s business finances.

Milestone payments through escrow guarantee funds availability and release payments only after verified work completion, reducing disputes and increasing contractor trust. The escrow agent acts as an independent referee, confirming that each phase of work meets the agreed standard before money changes hands.

Milestone payments vs. traditional payment methods

The table below compares milestone escrow payments against traditional upfront or progress payment methods:

| Payment Method | Fund Security | Dispute Risk | Verification Required |

|---|---|---|---|

| Milestone escrow | Funds held by neutral third party | Low | Yes, at each phase |

| Traditional progress billing | Funds in contractor’s account | Medium to high | Minimal |

| Full upfront payment | No protection after transfer | Very high | None |

| Net-30 invoicing | Delayed, no fund guarantee | Medium | Invoice-based only |

Traditional progress billing gives contractors access to funds before work is fully verified. Full upfront payment offers no recourse at all. Milestone escrow is the only method that ties every dollar to a confirmed deliverable.

Common milestones and how verification works

Typical milestones in a home renovation project include:

- Foundation or demolition complete: Verified by site inspection before framing begins

- Rough-in work approved: Plumbing, electrical, and HVAC rough-ins pass municipal inspection

- Drywall and insulation complete: Visual inspection confirms coverage and quality

- Substantial completion: Final walkthrough confirms all contracted work is done

- Punch list resolved: All deficiencies corrected before final payment releases

Each milestone release requires documented evidence, either a passed inspection report, signed completion form, or photographic record. This documentation also protects contractors by proving they completed work before payment was due, which reduces disputes from both sides.

Which digital payment methods reduce contractor payment fraud?

Modern contractor payment security depends on choosing the right payment technology and applying strict verification protocols. ACH transfers are the most common method for contractor payments, but they carry specific fraud risks that homeowners and project managers must understand.

Average ACH fraud loss in construction ranges from $25,000 to $50,000 per incident. The most common cause is redirected payments after a fraudster sends a fake banking change request by email. This is a preventable loss with one rule: always confirm banking changes by phone.

Secure payment options worth using

The most reliable safe payment methods for contractors combine technology with human verification:

- ACH with dual authorization: Requires two approvers before any payment processes, reducing single-point fraud risk

- Virtual cards with tokenization: Generate a unique card number for each transaction, so a compromised number cannot be reused

- Dedicated payment platforms: Tools like specialized payment platforms provide full project-to-payment visibility while preserving contractor supply chain confidentiality

- Escrow-integrated platforms: Release funds automatically when milestone conditions are met and verified

Payment platforms with real-time visibility increase supplier trust and reduce administrative friction. When contractors can log in and see exactly where a payment stands in the approval process, disputes drop and relationships improve. Transparency is not just good practice. It is a fraud deterrent.

How automation reduces human error in payments

Automating AP processes with AI reduces human error and payment delays while improving supplier relations through timely and accurate payments. For homeowners managing multiple contractors on a renovation, automated reminders, approval workflows, and payment tracking replace manual spreadsheets that are easy to mismanage. Platforms that integrate contract terms with payment schedules flag discrepancies before they become disputes.

Pro Tip: Set up a dedicated email address and phone number exclusively for contractor payment communications. This makes it immediately obvious when a message comes from an unexpected source, which is often the first sign of a fraud attempt.

How to integrate secure payments into your renovation workflow

Building a secure online contractor payment process into your project from the start takes planning. The steps below apply whether you are managing a single bathroom remodel or coordinating multiple contractors on a full home renovation.

-

Define payment terms in the contract. Every contract should specify the payment schedule, milestone definitions, acceptable payment methods, and the process for requesting changes. Verbal agreements on payment terms are unenforceable and create disputes.

-

Set up a dedicated project account. Keep renovation funds separate from your personal or business operating accounts. This makes tracking straightforward and limits exposure if fraud occurs.

-

Complete vendor onboarding before work starts. Collect W-9, ACH authorization, license verification, and insurance certificates before the first payment is authorized. Use IRS TIN Matching to confirm W-9 accuracy.

-

Establish a milestone verification process. Decide in advance who verifies each milestone, what documentation is required, and how long the approval takes. Write this into the contract so contractors know what to expect.

-

Track lien waivers at every payment stage. Collect a conditional lien waiver when you issue payment and an unconditional waiver after the payment clears. This progressive tracking protects you from subcontractor liens throughout the project.

-

Run compliance checks before final payment. Verify that all permits are closed, inspections are passed, and all lien waivers are collected before releasing the final milestone payment. This is your last point of leverage.

The table below summarizes the key documents and actions at each project payment stage:

| Project Stage | Required Document | Verification Action |

|---|---|---|

| Before work begins | W-9, ACH form, license, insurance | IRS TIN Match, license board check |

| First milestone | Conditional lien waiver | Site inspection or photo documentation |

| Mid-project payments | Progress lien waivers | Milestone completion sign-off |

| Substantial completion | Unconditional lien waiver | Final walkthrough, permit closure |

| Final payment release | All permits closed, punch list signed | Confirm all waivers collected |

For homeowners hiring contractors in Texas, hiring contractors securely involves additional state-specific licensing requirements that are worth reviewing before you sign any contract. Transparency in contractor selection also plays a direct role in payment security, since contractors who are open about their credentials and processes are statistically less likely to create payment disputes.

Key takeaways

A secure payment process for contractors requires vendor onboarding, escrow or milestone payment structures, and multi-channel fraud verification working together from project start to final payment.

| Point | Details |

|---|---|

| Onboarding prevents most fraud | Collect W-9, ACH forms, licenses, and insurance before authorizing any payment. |

| Escrow protects project funds | Neutral third-party escrow holds funds and releases them only after verified milestone completion. |

| Phone verification stops ACH fraud | Always confirm banking changes by phone; email-only requests are the leading fraud vector. |

| Lien waivers start at payment one | Collect conditional waivers with each payment and unconditional waivers after funds clear. |

| Automation reduces human error | AI-driven AP processes and payment platforms cut delays and improve contractor relationships. |

Why most homeowners get payment security backwards

I have reviewed hundreds of renovation projects where payment disputes were entirely preventable. The pattern is almost always the same. Homeowners focus intensely on choosing the right contractor and then treat the payment process as an afterthought. They hand over a large deposit, skip the paperwork, and assume a signed contract is enough protection.

The uncomfortable truth is that a signed contract without proper onboarding, lien waiver tracking, and verified payment methods is close to worthless in a dispute. Courts can enforce contracts, but recovering money already transferred to a contractor who has disappeared or gone bankrupt is a different matter entirely.

What actually works is treating the payment process as a parallel project to the renovation itself. Set it up before work starts. Document every step. Verify every change. The contractors who push back on escrow or lien waivers are telling you something important about how they operate.

I am also seeing a real shift in how homeowners approach this. Platforms that combine contractor vetting with transparent payment tracking are changing the dynamic. When a contractor knows their payment history and performance are visible to future clients, their behavior changes. New payment technologies are improving construction payment transparency, but they must be paired with the right verification protocols to avoid creating new vulnerabilities.

The homeowners who never have payment disputes are not lucky. They are organized. They collected the documents, set up the milestones, and confirmed every banking change by phone. That discipline is available to anyone willing to build it into their process from day one.

— Devin

How Bidwolf helps you hire and pay contractors with confidence

Finding a trustworthy contractor is hard enough without also worrying about payment fraud and documentation gaps. Bidwolf connects Texas homeowners with license-verified local contractors through a transparent bidding process that makes comparing credentials and payment terms straightforward.

When you post a project on Bidwolf, you receive competitive bids from vetted professionals who have already passed credential checks. The platform’s built-in messaging keeps all project communication in one place, which makes it easier to spot anything unusual before money moves. For homeowners who want to start with a cost estimate before committing to a contractor, Bidwolf’s project cost estimator gives you a realistic baseline for planning your payment milestones. Secure payments start with the right contractor. Bidwolf makes finding that contractor faster and safer.

FAQ

What is a secure payment process for contractors?

A secure payment process for contractors is a structured system that uses verified onboarding, milestone-based fund releases, and fraud prevention protocols to protect both homeowners and contractors. It typically includes escrow accounts, lien waiver tracking, and multi-channel payment verification.

How does escrow work for home renovation payments?

Escrow accounts hold project funds with a neutral third party and release payments only after verified milestone completion. This prevents contractors from accessing funds before work is confirmed and protects homeowners if a contractor faces financial trouble mid-project.

What is the biggest contractor payment fraud risk for homeowners?

ACH redirection fraud is the leading risk. It occurs when a fraudster sends a fake banking change request by email, and the homeowner updates payment details without phone verification. Average ACH fraud losses in construction range from $25,000 to $50,000 per incident.

Why do lien waivers matter in contractor payments?

Lien waivers confirm that a contractor or subcontractor has been paid and waives their right to place a lien on your property for that payment. Collecting them progressively at each payment stage protects homeowners from subcontractor liens even when the general contractor has already been paid.

What documents should I collect before paying a contractor?

Collect a completed W-9, a signed ACH authorization form, a valid contractor’s license, and a certificate of insurance naming you as an additional insured. Verify the W-9 through IRS TIN Matching and confirm the license through your state’s licensing board before authorizing any payment.